PCP Claims – Case Study

Personal Contract Purchase (PCP) agreements are a popular financing option in the UK car market, offering a flexible alternative to traditional finance.

Despite their popularity, PCP agreements have increasingly been at the centre of legal disputes, particularly concerning claims of mis-selling. This article explores the development of PCP claims, key legal precedents, recent regulatory updates and what the future holds for consumers and litigation funders.

The Rise of PCP Agreements

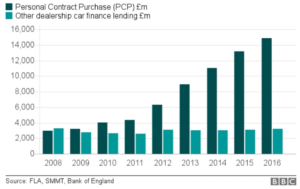

Since their introduction to the UK market in the early 2000s, PCP agreements have quickly gained popularity. Consumers were attracted by the opportunity to drive new vehicles without the financial commitment of outright ownership. With lower monthly payments and the flexibility to purchase, return, or trade in the vehicle at the end of the contract, PCP agreements became an appealing alternative to traditional finance.

By 2015, PCP agreements made up 76% of all new cars financed by personal consumers, according to Arc Ratings.

However, concerns about mis-selling soon followed. By 2016, consumers were reporting issues with unclear terms, particularly around balloon payments and hidden commission structures. Some dealers inflated interest rates to earn higher commissions without properly disclosing this to the consumer, sparking concerns about transparency and fairness in the market.

The Emergence of Mis-selling Claims

As awareness grew, so did the number of claims related to mis-sold PCP agreements. The Financial Ombudsman Service (FOS) reported a significant rise in complaints from consumers who felt misled by undisclosed costs and inflated interest rates. Discretionary commission arrangements, where dealers earned higher commissions by increasing interest rates, were a major concern. Industry estimates suggest that around 40% of PCP contracts signed before 2021 included discretionary commission provisions.

As these practices became more widely known, consumers increasingly sought redress. It became clear that many consumers were not receiving the full picture when entering these contracts, leading to a surge in legal actions aimed at holding dealers and lenders accountable for mis-selling.

Legal Precedent and the Impact of the Plevin Case

The Plevin v Paragon Personal Finance case in 2014 set an important legal precedent for PCP claims. The Supreme Court ruled that failing to disclose significant commissions could render a credit agreement unfair under the Consumer Credit Act 1974. This ruling initially applied to Payment Protection Insurance (PPI), opened the door for PCP claims where undisclosed commissions or a lack of transparency in financial agreements became grounds for legal action.

Regulatory Response – Timeline

2017

In response to growing concerns, the Financial Conduct Authority (FCA) launched an investigation into the motor finance market in 2017, with a particular focus on PCP agreements. The review highlighted significant issues with the way these agreements were sold, particularly regarding the lack of transparency in commission structures.

2020

By 2020, the FCA revealed that some dealers were inflating interest rates to earn higher commissions, a practice that did not align with the best interests of consumers.

2021

In January 2021, the FCA introduced new rules to ban discretionary commission models in PCP agreements, aiming to create a fairer and more transparent market. The FCA estimated these changes would save customers £165 million a year.

However, these changes did not resolve the historical issues associated with PCP agreements. As more consumers become aware of their rights, the number of claims related to historical mis-selling is expected to continue rising.

2024

Earlier in 2024, Lloyds Banking Group became the first UK bank to set aside £450 million to cover potential costs from the ongoing FCA investigation into mis-sold car finance agreements. Lloyds’ provision underscores the growing concern about the scale of misconduct within the motor finance sector.

In July 2024, the FCA announced that its review of historical PCP claims had been delayed until December 2025, providing more time to assess historical complaints and develop a comprehensive strategy.

While the delay aims to ensure a more thorough assessment, it also poses challenges for law firms and consumers. The postponement could lead to extended case resolutions and longer settlement times, potentially increasing both costs and frustration for all parties involved.

Looking Ahead: The Future of PCP Claims

The future of PCP claims is set to focus largely on historical mis-selling cases. Despite the FCA’s 2021 regulatory reforms, claims related to older agreements are expected to drive claims for years to come as many consumers are only now discovering that they may have been mis-sold PCP agreements, particularly regarding undisclosed commissions and inflated interest rates.

As awareness grows, so will the number of claims. A redress scheme, similar to the PPI mis-selling scandal, may be necessary to address widespread mis-selling practices in PCP agreements. It is projected that the FCA’s investigation could uncover billions of pounds in overcharged interest, with individual consumers potentially eligible for compensation averaging around £1,100.

The Role of Litigation Funding in PCP Claims

Litigation funding is important in helping consumers pursue claims related to mis-sold PCP agreements. The financial burden of legal action can be a significant barrier, and funding ensures that consumers can challenge unfair practices and seek compensation without upfront costs.

At Fenchurch Legal, we recognise the strength of many PCP claims and see the potential for this to become a significant area of consumer litigation. While our current exposure remains minimal, we are closely monitoring the FCA’s ongoing review, expected to conclude in 2025. Once the findings are released, we will reassess our position, aligning with the regulatory landscape and exploring strategic litigation funding to support valid claims.

Sources:

[1] https://arcratings.com/researches/uk-car-finance-personal-contract-purchase-pcp-spotlight/#:~:text=PCP%20agreements%20were%20first%20introduced,2016%20from%2045.8%25%20in%202009.

[2] Car finance FREE reclaim tool & guide | MSE (moneysavingexpert.com)

[3] https://www.fca.org.uk/news/news-stories/our-work-motor-finance

[4] https://www.fca.org.uk/news/press-releases/fca-ban-motor-finance-discretionary-commission-models

[4] https://www.fca.org.uk/news/press-releases/fca-ban-motor-finance-discretionary-commission-models

[5] https://www.itv.com/news/2024-02-22/lloyds-sets-aside-450m-over-mis-sold-car-finance-investigation

[6] https://www.fca.org.uk/news/statements/update-motor-finance-work

[7] https://www.driving.co.uk/car-clinic/advice/car-finance-mis-selling-scandal-are-you-due-over-1000-compensation-from-a-pcp-or-hp-deal/